How do you to Calculate Settlement Discounts?

PLEASE NOTE, HMRC INTRODUCED NEW RULES IN APRIL 2015 – TO UPDATE YOURSELF ON THE NEW RULES, PLEASE SEE OUR BLOG HERE

Whilst there are new rules in place, you still have to know how to calculate settlement discounts (now known as Prompt Payment Discounts), so hopefully you will still find this BLOG helpful.

Settlement discounts are generally offered to credit customers as a means of encouraging them to pay their invoices quickly. It is up to us to decide what the payment terms will be e.g. we could offer a customer a 3% settlement discount if they pay within 14 days, or perhaps a 5% discount if they pay within 7 days, and so on. It is then up to the customer to decide whether or not to take advantage of the settlement discount offered.

VAT Implications

VAT on an invoice is ALWAYS calculated after ALL discounts have been taken, even if the customer subsequently doesn’t take advantage of a settlement discount.

A commonly asked question is “well, what happens if the customer decides not to take the settlement discount i.e. because the VAT amount will be lower than usual, does this have to be adjusted for?”

The answer at the moment is ‘NO’. HMRC are aware that it would be a costly exercise to go back through all the invoices to see who did and who did not take advantage of the settlement discounts and costlier still to adjust and re-issue some of the invoices. Having said that, they are currently planning to change the rules on this after 31 March 2015 – watch this space! (As the day after 31 March is 1 April, we will need to wait to see if this is an April Fool!!)

Settlement Discount Calculation Example 1

Joel purchases goods for £400 + VAT. Joel is offered a 5% settlement discount if he pays within 10 days.

- a) How much will Joel pay if he pays within 10 days?

- b) How much will Joel pay if he DOES NOT pay within 10 days?

Here is the invoice extract:

So how is the VAT calculated?

The settlement discount calculation is NOT shown on the invoice – you need to use a bit of scrap paper to work this out.

Firstly, start off with the net amount of £400 and multiply this by 5%

i.e. £400 x 5 / 100 = £20 OR £400 x 0.05 = £20. The £20 is your settlement discount amount.

Next, deduct the £20 from the £400 net total i.e. £400 – £20 = £380

This £380 is the amount that you will calculate the VAT amount on

i.e. £380 x 20 / 100 = £76 OR £380 x 0.20 = £76.

Record the £76 on the invoice, then add this amount to the £400 net total which equals a total amount payable of £476

i.e. £400 + £76 = £476.

Settlement Discount Example 1 Answers

In answer to our questions a) and b) above:

- If Joel pays the invoice within 10 days, HE will need to deduct the settlement discount amount of £20 from the invoice total. So, Joel will pay £456 if he pays the invoice within 10 days (i.e. £476 – £20)

- If Joel does NOT pay the invoice within 10 days, then he will need to pay the total amount as shown on the invoice i.e. £476

Settlement Discount Calculation Example 2

Faye purchases goods for £575 + VAT. Faye is offered a 10% trade discount and a 4% settlement discount if she pays within 14 days.

- How much will Faye pay if she pays within 14 days?

- How much will Faye pay if she DOES NOT pay within 14 days?

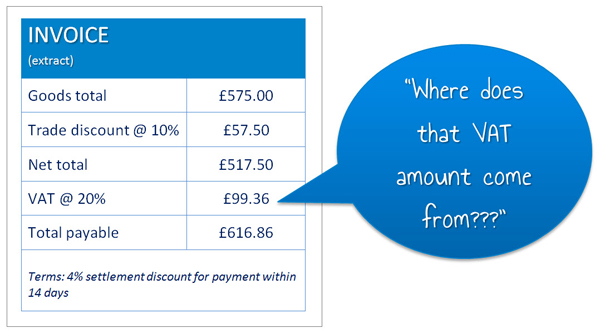

Here is the invoice extract:

This time, we need to start off with the trade discount calculation.

Take the goods total of £575.00 and multiply this by 10%

i.e. i.e. £575.00 x 10 / 100 = £57.50 OR £575 x 0.10 = £57.50

Deduct the trade discount of £57.50 from the goods total amount of £575.00.

i.e. £575.00 – £57.50 = £517.50. This figure is our net amount.

Next, we have to calculate the settlement discount, and again, this calculation is NOT shown on the invoice – you need to use a bit of scrap paper to work it out.

Take your net amount of £517.50 and multiply this by 4%

i.e. £517.50 x 4 / 100 = £20.70 OR £517.50 x 0.04 = £20.70. The £20.70 is your settlement discount amount.

Deduct the £20.70 from the £517.50 net total i.e. £517.50 – £20.70 = £496.80

This £496.80 is the amount that you will calculate the VAT amount on

i.e. £496.80 x 20 / 100 = £99.36 OR £496.80 x 0.20 = £99.36.

Record the £99.36 on the invoice, then add this amount to the £517.50 net total which equals a total amount payable of £616.86

i.e. £616.86 + £99.36 = £616.86.

Settlement Discount Example 2 Answers

In answer to our questions a) and b) above:

- If Faye pays the invoice within 14 days, SHE will need to deduct the settlement discount amount of £20.70 from the invoice total. So, Faye will pay £596.16 if she pays the invoice within 14 days (i.e. £616.86 – £20.70).

- If Faye does NOT pay the invoice within 10 days, then she will need to pay the total amount as shown on the invoice i.e. £616.86.

A Common Error in AAT Settlement Discount Questions

A common error that can arise is when students are given an invoice extract and are asked what the settlement discount amount will be. Mistakenly, some students will calculate the settlement discount from the invoice total amount rather than calculating it based on the invoice net amount, so watch out for this one!

Important Notes About Posting Settlement Discounts

Here are some important notes about posting settlement discounts to the accounts:

- Settlement discounts are NEVER recorded in the Sales Day Book where we record all the sales invoices sent to our credit customers. When the invoices are entered in the Sales Day Book, we don’t know at this stage whether or not the customer will in fact take advantage of a settlement discount. So, simply record the Net, VAT and Total amounts as shown on the invoice.

- Settlement discounts are accounted for when the customer pays us. We will know at this point, whether or not the customer took advantage of the settlement discount. When posting the cash book (see cash book blog here), the settlement discount should be recorded as a DEBIT entry in the Discounts Allowed Account and a CREDIT entry in the Sales Ledger Control Account (SLCA)

- Something that is regularly forgotten is to remember to record the settlement discount in the customer’s Sales Ledger account. This should be recorded (along with the receipt) to the CREDIT side of the Sales Ledger Account.

- Another entry often forgotten is when you come to prepare a customer Statement of Account. It is important to remember to record the settlement discount here too, otherwise the outstanding balance on the customer statement will be incorrect i.e. the amount due will be too high (and you won’t have a very happy customer!)

I hope this helps – if you have any further questions though, please contact us here.

We hope that these study tips have helped you! Whilst we are not able to respond to any specific questions you might have about our posts, do please let us know if there are any further topics you would like us to write about. If, however, you are one of our tutor supported students, please get in touch with your personal tutor who will be more than happy to help you.