Other Stuff

UK Small Business Week

Why Investing in Yourself Can Open New Opportunities Small businesses are the backbone of communities across the UK. From independent retailers and local service providers to growing accountancy firms and

Why Investing in Yourself Can Open New Opportunities Small businesses are the backbone of communities across the UK. From independent retailers and local service providers to growing accountancy firms and

A humorous look at revision, memory, exam stress, and why your brain remembers awkward moments more easily than accounting formulas If you can still vividly remember tripping over in Year

Fuel Your Brain for Smarter Study Flexible learning gives people the opportunity to study around work, family life, and existing commitments. It also gives students unrestricted access to their kitchen,

What the Salary Survey Reveals About Your Future in Finance If you have ever wondered where an accountancy qualification could take you, the latest AAT Salary Survey 2025 offers a

Everything You Need to Know Before Starting a Distance Learning Course If you’re thinking about starting a distance learning accountancy course, chances are you’ve got a few questions. In

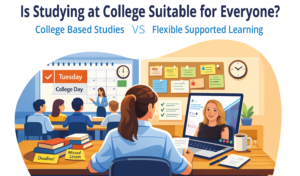

Why distance learning can be a more flexible way to study AAT and bookkeeping For a lot of people, studying at college feels like the “normal” route. You pick a