Journals – one of the trickiest topics in double entry bookkeeping! Which account gets debited and which account gets credited?

There are two types of journals, primary and secondary. Secondary journals are the ones we use to post entries from the Books of Prime Entry into the General Ledger e.g. to post the Cash Payments Book, the secondary journal might look like this:

Primary journals are those that cannot be entered into the accounting records in any way other than by preparing a journal i.e. they can’t be entered in any of the Books of Prime Entry e.g. Irrecoverable (Bad) Debts, Depreciation, Prepayments, Accruals and of course journals to correct errors. We will focus on the journals to correct errors.

These journals are used where we know we have made a mistake in the accounts (e.g. we have prepared a Trial Balance and the two totals don’t agree).

Here are some examples:

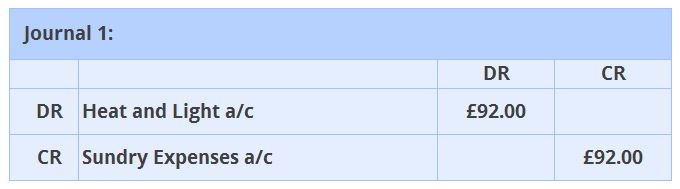

- An amount of £92 has been debited to the sundry expenses account instead of the heat & light account.

- A payment to a trade creditor has been entered into the purchases ledger control a/c and cash book as £1,420 instead of £1,240.

- An entry to record discounts received of £64 has been reversed, so it has been debited to discounts received and credited to the PLCA.

The first step to take for each of these journals is to identify which two accounts in the General Ledger are going to be affected.

So, looking at Journal 1 first then:

Journal 1.

This one is fairly straight forward – the two accounts affected are the sundry expenses account and the heat & light account. Here we have accidentally recorded £92 in the sundry expenses account instead of the heat & light account, so, we have to remove it from the sundry expenses account and enter it into the heat & light account. These two accounts are both expense accounts, therefore the amount will have been recorded as a debit entry to the sundry expenses account (the credit entry will have been the Bank, or the PLCA dependant on whether the amount has be paid or is still outstanding for payment – we’ll assume we’ve paid the bill, so the credit entry would be the Bank.)

- DR Sundry Expenses

- CR Bank

No mention has been made about the Credit entry, so the assumption is that this side of the double entry is correct, so we only need to correct the Debit entry.

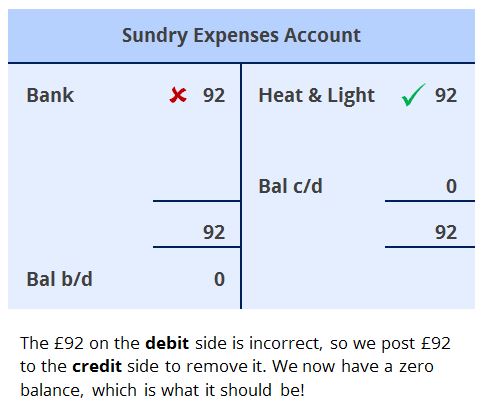

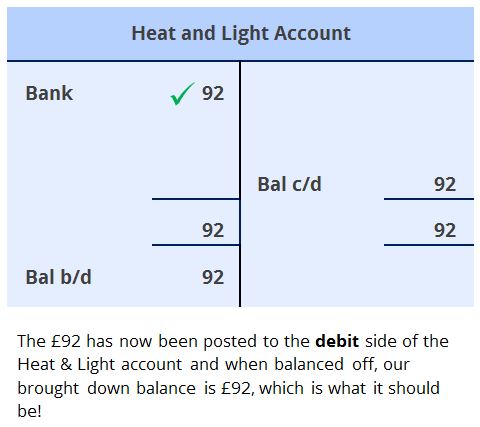

A really useful way to check if your journal entries are correct is to draw up mini T-accounts. Firstly record the incorrect entry, then record the entry as you think it should be and finally balance off the accounts. Are the brought down balances as you expected them to be?

Here’s how the T-accounts will be affected in Journal 1:

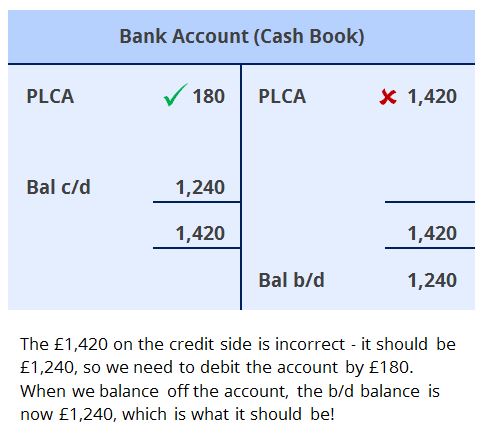

Journal 2.

A payment to a trade creditor has been entered into the purchases ledger control a/c and cash book as £1,420 instead of £1,240.

Looking at the two accounts that are involved with this error, we can firstly see that the Purchases Ledger Control Account (PLCA/Payables/Creditors) is affected. The other account affected is the cash book (note that as far as the AAT is concerned, the cash book is effectively the bank account – this is why you are rarely ever given a bank T-account in the General Ledger; the cash book is the bank.)

So, in this example, the person recording the entry has got their numbers muddled up. The difference between £1,420 and £1,240 is £180, so £180 too much has been recorded for this payment. This means that we have to reduce the bank account by £180 and increase the PLCA by £180 (to increase what is owed i.e. we didn’t pay off as much as we thought we had). The PLCA is a liability of the business – an increase in a liability is a credit entry (seeDeadClic). This will be the journal entry to make the correction:

Here’s how the T-accounts will be affected in Journal 2:

Please note that on the Bank account you would normally hope to have a Debit b/d balance (indicating that we have money in the bank, rather than an overdraft). On the PLCA, we would always have a Credit b/d balance (indicating that we owe our suppliers ‘x’ amount of money). Each account would normally have an opening balance, which is not shown in these T-account examples.

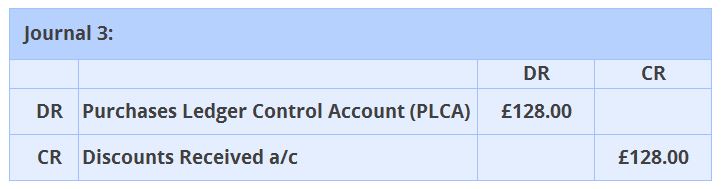

Journal 3.

An entry to record discounts received of £64 has been reversed, so it has been debited to discounts received and credited to the PLCA.

Looking at the two accounts that are involved with this error, clearly we can see that the Purchases Ledger Control Account (PLCA/Payables/Creditors) and Discounts Received a/c are affected.

In this error, we have recorded the PLCA amount of £64 on the credit side instead of the debit side and we have recorded Discounts Received (a decrease in an expense) as a debit rather than a credit, so we simply need to reverse this. Here is the journal to correct the error:

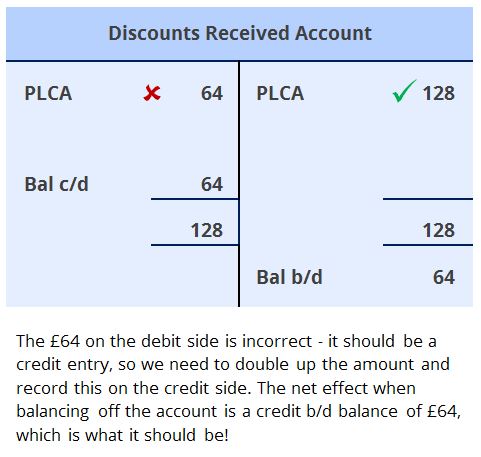

Why is the amount £128 instead of £64? Well, the first £64 removes the error (so that you end up with a zero balance) and the second £64 puts the amount where it should be. This is better illustrated in the T-accounts shown below:

I hope that this de-mystifies things a little for you!

As mentioned at the beginning, dealing with journals can be tricky! If you would like to know more about journals, you might want to consider our AAT Foundation Certificate in Bookkeeping course (via distance learning). You can read more about the course HERE:

We hope that these study tips have helped you! Whilst we are not able to respond to any specific questions you might have about our posts, do please let us know if there are any further topics you would like us to write about. If, however, you are one of our tutor supported students, please get in touch with your personal tutor who will be more than happy to help you.